When you fill a prescription for a Medicare Part D drug, you might assume your pharmacist will give you exactly what your doctor ordered. But that’s not always the case. Medicare Part D substitution - the process of swapping one drug for another - happens more often than most beneficiaries realize. And it’s not just about saving money. It’s about rules, tiers, and what your specific plan allows.

How Substitution Works in Medicare Part D

Substitution in Medicare Part D isn’t the same as what happens with over-the-counter meds. You can’t just ask for a cheaper version and walk out. It’s governed by your plan’s formulary - a list of approved drugs - and how that list is organized into tiers. Most plans use a five-tier system:

- Tier 1: Preferred generics (lowest cost)

- Tier 2: Non-preferred generics

- Tier 3: Preferred brand-name drugs

- Tier 4: Non-preferred brands (and some generics)

- Tier 5: Specialty drugs (highest cost)

If your doctor prescribes a Tier 3 brand-name drug, your pharmacist might automatically switch you to a Tier 1 generic - if it’s therapeutically equivalent and allowed under your plan’s rules. This is called generic substitution, and it’s encouraged because it cuts costs for everyone. But if your drug is on Tier 4 or 5, the plan may require prior authorization before allowing a swap. Some plans even block substitution entirely for certain drugs, especially if they’re biologics or have narrow therapeutic windows.

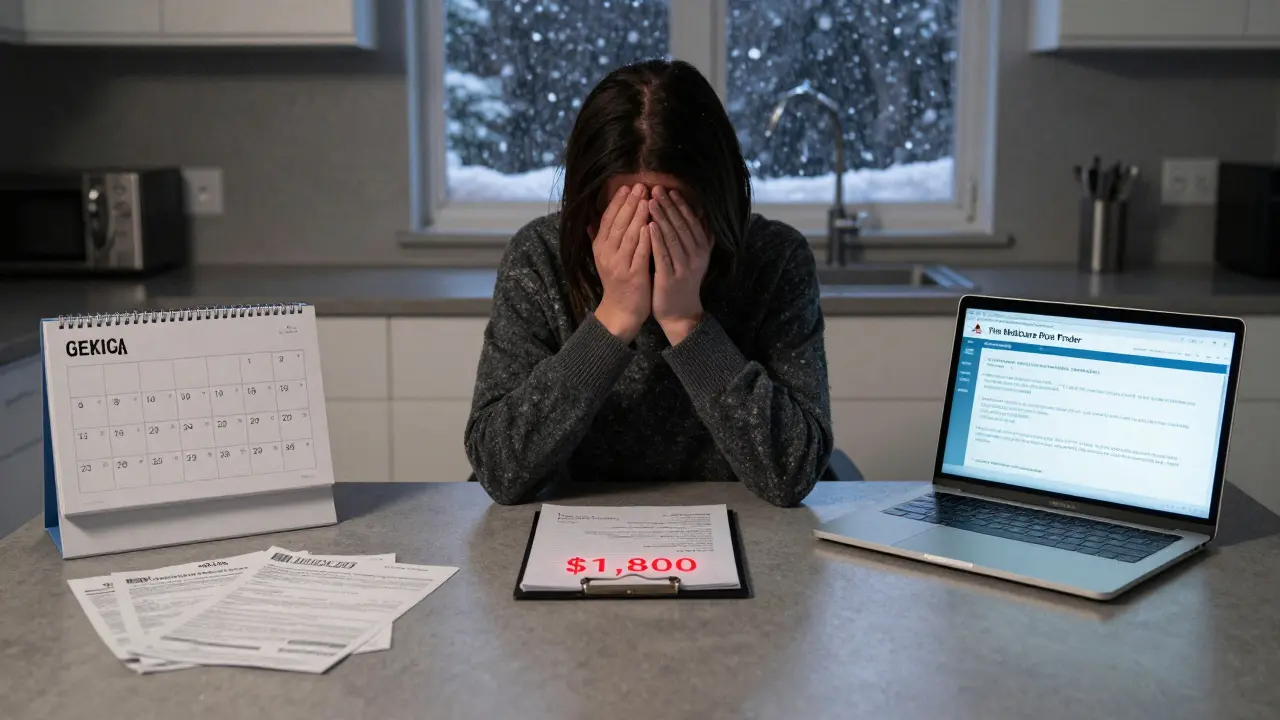

The $2,000 Out-of-Pocket Cap Changes Everything

Before 2025, beneficiaries hit a notorious "donut hole" - a coverage gap where they paid 100% of drug costs until they spent enough to qualify for catastrophic coverage. That gap is gone. As of January 1, 2025, the maximum you pay out-of-pocket for covered Part D drugs is $2,000. Once you hit that number, you enter catastrophic coverage, and you pay nothing for the rest of the year.

This change reshapes substitution logic. Before, people might avoid switching drugs to keep costs low before the donut hole. Now, if you’re nearing $2,000, the system pushes you toward cheaper alternatives - not because of plan rules, but because it’s in your best interest. If you’re on a $500-a-month specialty drug and you’ve already spent $1,800, your plan may push you toward a biosimilar or generic alternative to avoid hitting the cap too early. The goal? Keep you covered without surprise bills.

Who Decides What Gets Substituted?

It’s not your doctor. It’s not always your pharmacist. It’s your plan’s Pharmacy Benefit Manager (PBM). These are private companies hired by Medicare Part D insurers to manage drug lists, negotiate prices, and set substitution rules. PBMs decide:

- Which drugs are on your formulary

- Which tier they’re placed in

- Whether generic substitution is allowed

- When step therapy or prior authorization is required

For example, one plan might allow substitution between two different blood pressure drugs in the same class. Another might require you to try a cheaper option first - even if your doctor says it won’t work for you. That’s called step therapy. If you’ve been on a drug for years and your plan suddenly removes it from the formulary, you’ll get a notice. You can appeal, but until then, you may be forced to switch.

Plan Differences Matter - A Lot

In 2025, there are only 14 stand-alone Medicare Part D plans (PDPs) available on average nationwide - down 52% from a decade ago. But 34 Medicare Advantage plans (MA-PDs) include drug coverage. These integrated plans often have different substitution rules than traditional PDPs.

Why? Because MA-PDs bundle medical and drug benefits. If your plan covers both your heart medication and your doctor visits, they have more incentive to keep you on a drug that prevents hospitalization - even if it’s more expensive. Meanwhile, stand-alone PDPs only care about drug costs. That means substitution may be more aggressive.

And here’s the catch: no two plans are the same. A drug covered at Tier 1 in Plan A might be Tier 4 in Plan B. One plan might allow substitution for insulin, another might not. Humana caps insulin costs at $35 per 30-day supply - but only if you’re on their approved formulary. If you’re on a different plan, you might pay $150. That’s not a substitution - that’s a coverage gap.

What You Can Do to Protect Yourself

Don’t wait until you’re at the pharmacy counter to find out your drug was swapped. Here’s what you need to do:

- Review your formulary every year. During Open Enrollment (October 15-December 7), log into your plan’s website and search for every drug you take. Don’t trust memory. Plans change their lists without notice.

- Check for step therapy rules. If your plan requires you to try a cheaper drug first, ask your doctor if they’ll write a letter of medical necessity. Many do.

- Ask your pharmacist to explain the swap. If you get a different pill, ask: "Is this a substitution? Why? Is it the same as what my doctor prescribed?" If they say "It’s covered," ask: "Is it on the same tier?"

- Use the Medicare Plan Finder. Enter your exact drugs and dosage. It shows you which plans cover them and at what cost. Don’t just pick the cheapest premium.

- Know your out-of-pocket tracking. Keep a simple log of what you pay each month. Once you’re close to $2,000, you can push back on non-essential substitutions.

What Happens If You’re Forced to Switch?

Some drugs don’t have good substitutes. If you’re on a biologic for rheumatoid arthritis, switching to a biosimilar might be fine. But if you’re on a drug for epilepsy or depression, even a small change can trigger seizures or mood crashes. If your plan forces a substitution that doesn’t work:

- File an exception request with your plan. You need a letter from your doctor explaining why the original drug is medically necessary.

- Request an expedited review. If your health is at risk, you don’t have to wait 30 days.

- Appeal if denied. You have the right to a second review by an independent third party.

Many people give up here. But 60% of appeals for drug coverage exceptions are approved - if you follow the steps. Don’t assume you’re stuck.

Looking Ahead: What’s Changing in 2026?

The $2,000 out-of-pocket cap increases to $2,100 in 2026. That means the "sweet spot" for substitution shifts slightly. PBMs will likely adjust formularies to push more drugs toward generics before you hit the cap. Expect more plans to include insulin and other high-cost drugs on Tier 1 - not because they’re cheap, but because the law requires it.

Also, more Medicare Advantage plans will include pharmacy networks that limit substitution to specific pharmacies. If your local pharmacy isn’t in-network, even a generic substitution might be blocked. That’s new. And it’s going to confuse people.

The bottom line? Medicare Part D substitution isn’t a simple swap. It’s a system built on cost, control, and complexity. But you’re not powerless. You have rights. You have tools. And with the right info, you can make sure you get the drug you need - not just the one your plan prefers.

Can my pharmacist substitute my brand-name drug for a generic without telling me?

No. Under Medicare Part D rules, pharmacists must inform you if they’re substituting a drug, even if it’s allowed by your plan. You have the right to refuse the swap and request the original prescription. If they don’t tell you, ask. If they still won’t tell you, contact your plan’s customer service - this is a violation of transparency rules.

Why does my plan cover my drug one year but not the next?

Plans update their formularies annually. PBMs negotiate new prices, and drug manufacturers may change pricing or availability. If your drug is removed, you’ll get a notice by October 1. You can appeal, switch plans during Open Enrollment, or ask your doctor for an alternative. Don’t ignore the notice - it’s your only warning.

Is insulin always covered under Part D?

Yes - but only up to $35 per 30-day supply. Since 2023, the Inflation Reduction Act capped insulin costs at $35 for all Part D plans. However, this applies only to insulin products listed on your plan’s formulary. If your plan doesn’t cover your specific insulin brand, you may still pay more. Always check your plan’s formulary for insulin coverage.

Can I switch Part D plans mid-year if my drug is no longer covered?

Usually, no. Open Enrollment is the only time you can switch. But if your plan removes your drug from the formulary, you qualify for a Special Enrollment Period. You can change plans immediately. Contact Medicare at 1-800-MEDICARE or your plan’s customer service to confirm eligibility.

Do all Medicare Advantage plans have the same substitution rules as stand-alone Part D plans?

No. Medicare Advantage plans (MA-PDs) often have tighter control over substitutions because they manage both medical and drug benefits. They may limit you to specific pharmacies or require you to use their preferred providers. Stand-alone Part D plans focus only on drug cost, so they’re more likely to push generic swaps. Always compare the formularies side-by-side before choosing.

Rachidi Toupé GAGNON

February 10, 2026 AT 12:34Pat Mun

February 10, 2026 AT 14:32Sophia Nelson

February 11, 2026 AT 22:46Skilken Awe

February 12, 2026 AT 22:55Kristin Jarecki

February 14, 2026 AT 04:08Suzette Smith

February 15, 2026 AT 05:51andres az

February 15, 2026 AT 06:39Autumn Frankart

February 15, 2026 AT 17:11Stephon Devereux

February 17, 2026 AT 04:42Steve DESTIVELLE

February 19, 2026 AT 03:03steve sunio

February 19, 2026 AT 21:38